Back in 2016 I wrote a long post about biodiesel, explaining what it is made from (mostly vegetable oil) and arguing that EPA should show restraint in setting targets for biodiesel because of the limited availability oils and fats and the harmful consequences of drawing too heavily from these limited sources. The world has changed in many ways since 2016, but the large-scale diversion of vegetable oil from food to fuel remains a bad idea. Now it is California policymakers’ turn to establish sensible guardrails on fuel policies to avoid creating problems in California, and around the world.

Since 2016, EPA has generally shown restraint in setting targets for biodiesel and related fuels, insofar as the law allows, and biodiesel consumption has actually fallen. But in its place renewable diesel is booming, produced in large oil refineries retrofitted for the purpose and consumed primarily in California. Biodiesel and renewable diesel are closely related fuels made from the same oils and fats, which remain scarce, expensive, and linked to deforestation and food price spikes.

For this reason, it is important that policy makers, not only at EPA but also in California, are realistic about the sustainably available supply of oils, and implement fuel policies to avoid excessive diversion of vegetable oil into transportation fuel production. The idea that a large number of oil refineries can keep humming along by replacing petroleum diesel with vegetable oil or used cooking oil is a dangerous illusion. Biofuels can play a productive role when used at a sustainable level. But we need to be realistic about where they come from, and limit feedstocks to sustainable resources used at a reasonable scale to avoid turning a helpful tool into a harmful dead end.

This article draws heavily from a series of articles on the Renewable Diesel Boom by Maria Gerveni, Scott Irwin and Todd Hubbs at farmdoc daily that I heartily recommend for more quantitative economic analysis. The conclusions and policy recommendations are purely my own.

Biodiesel and renewable diesel are mostly made from vegetable oil

Biodiesel and renewable diesel are made from the same starting materials, are both blended into diesel fuel, and are supported by the same regulations. Collectively biodiesel and renewable are referred to as bio-based diesel, which is especially relevant when considering the availability of oils and fats.

More than 80 percent of bio-based diesel is made from vegetable oil (the rest is mostly animal fats). The soybean and canola oil that make up the majority of biodiesel is basically the same as the cooking oil you buy at the grocery store, while the corn oil is mostly an inedible byproduct of ethanol production that is generally used for animal feed and other purposes. Yellow grease is a catch all term that includes used cooking oil as well as lower quality tallow from rendering facilities.

Using more oils and fats for fuel instead of food and animal feed has consequences for competing users of these products and for the global agricultural system. Of particular importance from a climate perspective is the relationship between rising use of oils and fats for fuel in the United States and soybean expansion in South America and palm oil expansion in Southeast Asia, both of which are major drivers of deforestation and global warming pollution. Figure 1 above shows that palm oil itself is not a significant direct source of US biofuel production. However, there are important indirect links between how much soybean oil bio-based diesel we use in the US and how quickly palm oil plantations expand in Indonesia or Malaysia. I’ll get to these connections shortly, but first, let’s consider the relationship between biodiesel and renewable diesel.

Renewable diesel is the fastest growing part of the US biofuel market

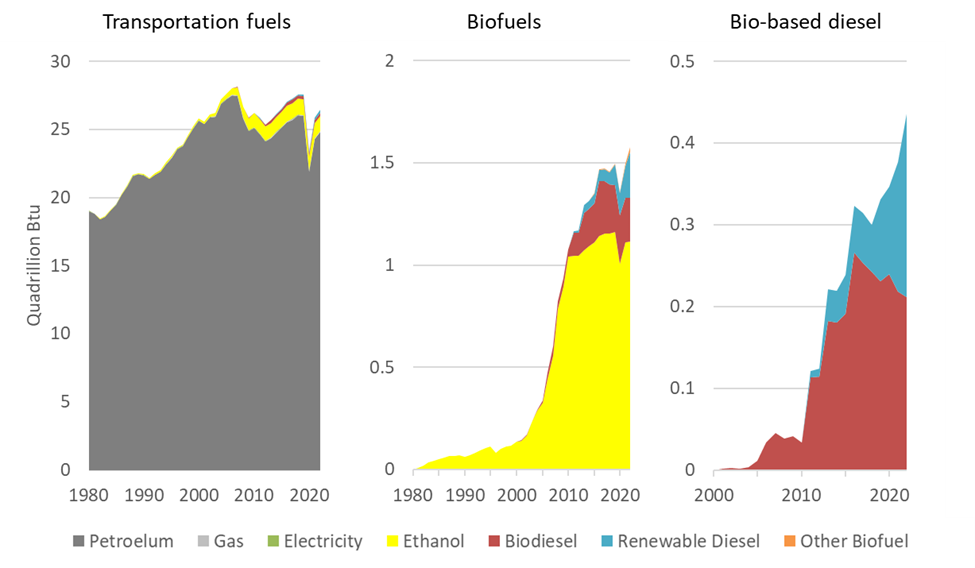

Biofuels overall account for a small but growing share of US transportation energy. Figure 2 shows that petroleum supplies 94 percent of US transportation energy while biofuels are 6 percent. Of the biofuels, ethanol, biodiesel and renewable diesel make up 70, 13 and 14 percent respectively. Ethanol consumption grew rapidly between 2000 and 2010 but after 2010 biodiesel took over as the major source of biofuel growth before being eclipsed by renewable diesel after 2016.

Biodiesel versus renewable diesel

Biodiesel and renewable diesel have several similarities and a few key differences. Both fuels are made from vegetable oils and fats and are blended into diesel fuel. Both fuels satisfy the requirements of the Federal Renewable Fuel Standard (RFS), which requires oil companies to blend biofuels into the gasoline and diesel they sell. So, in that sense biodiesel and renewable diesel compete for both feedstock and customers.

Biodiesel = an additive blended into diesel

Renewable diesel = a replacement for diesel fuel

Bio-based diesel = biodiesel + renewable diesel

Although biodiesel and renewable diesel are derived from the same feedstocks, the processes used to make them are different. Renewable diesel production uses a hydrogen treatment to remove oxygen from the fats and oils, while biodiesel is produced by a less complex process and retains some oxygen.

Renewable diesel, like fossil diesel, is a pure hydrocarbon and is so similar to fossil diesel that they can be used interchangeably. That is why renewable diesel is often described as a “drop in” fuel. By contrast, biodiesel is limited to specific maximum blends (usually 5 or 20 percent) and higher blends must be specially labeled and their use is limited to compatible vehicles.

The hydrogen treatment used to remove oxygen from the fats and oils increases the costs of renewable diesel production, but adds flexibility, so the latter may be produced from animal fats that are less readily made into biodiesel.

These differences also connect to historical and geographical differences. The growth of the biodiesel industry was promoted by soybean producers as a way to expand the market for soybean oil. As such it is not surprising that the Midwest has 70% of U.S biodiesel capacity, which is primarily in Iowa, Missouri, Illinois, and Indiana.

The renewable diesel industry is less centralized, but the largest share of production capacity, 60 percent, is in the Gulf Coast states, primarily Louisiana and Texas. US renewable diesel production was initially linked to animal fat. Tyson Foods helped launch a Renewable Diesel facility in Geismar, Louisiana that started up in 2010 as the first large US producer of renewable diesel made from animal fat.

More recently, much of the growth in renewable diesel has been from converted oil refineries, which already have the facilities for hydrogen treatment as well the logistics to receive trains or tanker ships of incoming oil (fossil or vegetable) and ship out finished diesel fuel. The oil industry increasingly controls bio-based diesel fuel production. Among other links, in 2022 Chevron purchased the largest biodiesel producer in the US, the Renewable Energy Group, and Marathon Petroleum and Phillips 66 are converting oil refineries to produce renewable diesel.

Perhaps the most notable difference between biodiesel and renewable diesel is that since 2016 renewable diesel consumption has been booming while biodiesel consumption has been declining. Biodiesel consumption in the US peaked in 2016, and by 2022 had declined 24 percent, while renewable diesel use has risen rapidly, growing almost 4-fold between 2016 and 2022. In 2022 renewable diesel surpassed biodiesel for the first time and combined the two sources of bio-based diesel now account for 7.3 percent of US diesel fuel consumption by volume.

Renewable diesel is (mostly) a California story

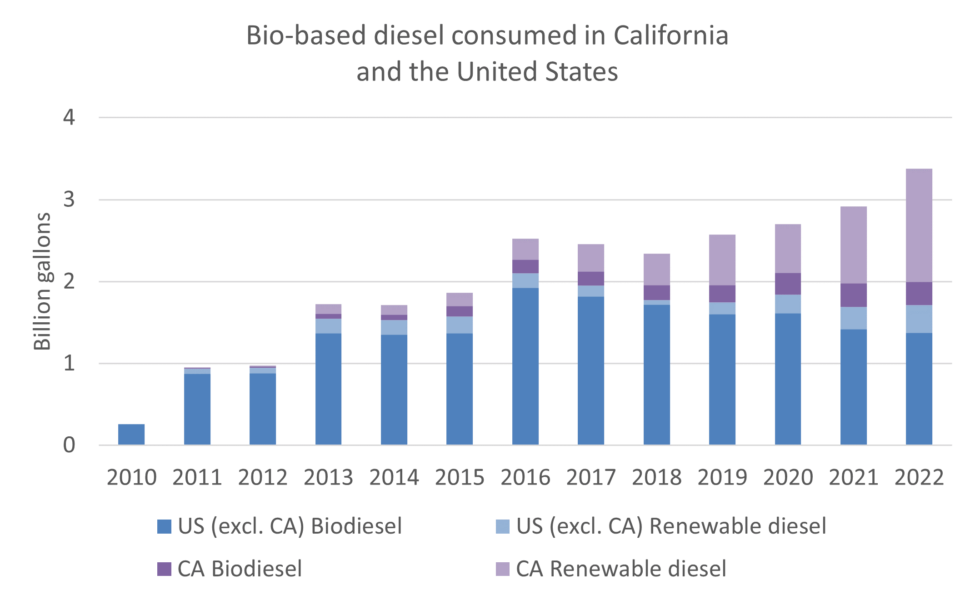

Most of the renewable diesel consumed in the United States is consumed in California (Figure 3). The concentration of renewable diesel in California is partly the result of California’s Low Carbon Fuel Standard policy, discussed later in this post. In 2022 California consumed half of US bio-based diesel. Rising California consumption has come partly at the expense of biodiesel consumption elsewhere in the US, which fell 28% percent in 2022 compared to its peak in 2016.

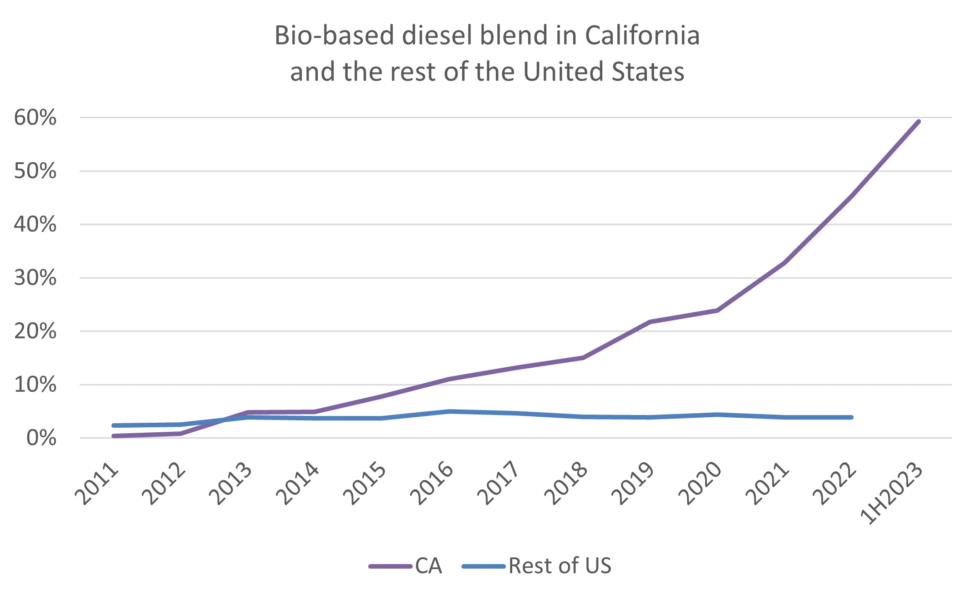

The blend rate of bio-based diesel in California is rising rapidly. In the first half of 2023, the combined share of renewable diesel and biodiesel rose to 59 percent of total diesel fuel use in California. Outside of California the share of bio-based diesel has fallen from 5 percent in 2016 to only 3.8 percent in 2022. A recent analysis from researchers at the University of California Davis found a 50 percent chance that petroleum diesel would disappear from California by 2028.

Renewable diesel production capacity is poised to grow rapidly

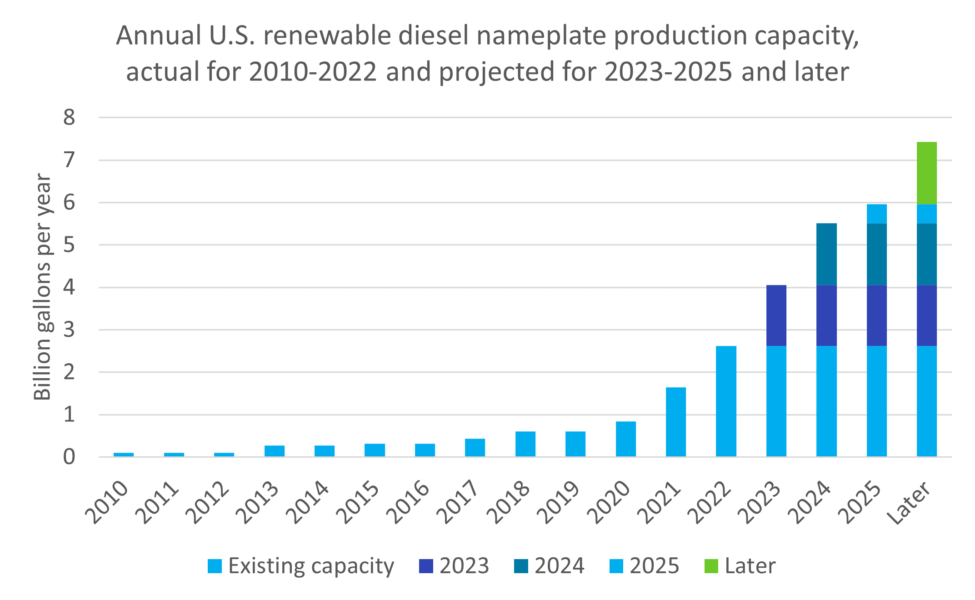

Renewable diesel production capacity in the United States is in the middle of a massive expansion. Production capacity grew by 400 percent between 2019 and 2022 and based on announced and planned projects, it could double again by the end of 2024. The figure below from a recent analysis of farmdoc daily, March 29, 2023 illustrates the massive, planned capacity buildout for renewable diesel. Whether all these facilities get built and operate at their full capacity depends a lot on policy decisions in California, DC and elsewhere.

California is at the eye of the storm, both as the main driver of demand and soon as a major producer as well. Two thirds of the capacity planned for 2023 and 2024 is in California, especially two projects in the San Francisco Bay area, the Marathon Martinez and Phillips 66 Rodeo refineries. These two facilities plan to bring on-line capacity of more than 1.4 billion gallons by the end of 2024.

Converted oil refineries

An important caveat to keep in mind when looking at renewable diesel capacity growth announcements, both recent and planned, is that the renewable diesel production facilities are generally not new facilities being built from the ground up for renewable diesel production. Many are oil refineries being converted from fossil fuel production to renewable fuel production. Petroleum refineries are massive compared to biofuel facilities. The difference in scale reflects both the larger scale of the demand for petroleum fuel and the economies of scale associated with the required facilities and infrastructure, including pipelines and ports to offload crude from tankers. Biofuel production facilities have generally been built on a smaller scale, reflecting the economic advantage of producing the fuel closer to where the vegetable oil or animal fat is produced.

Because oil companies are converting facilities they already have, the decision on capacity is based in part on the scale of the facilities they are converting. If these were new construction projects, the massive capacity expansions might be interpreted as reflecting a strong belief by investors that demand is likely to expand a commensurate amount, otherwise it would be foolish to invest their money. But for an oil company with an excess refining capacity, the decision to convert to renewable diesel may have a much lower threshold, and the capacity may be a function of the capacity of the existing infrastructure as much as a bet of new money on the scale of a new opportunity.

Another motivation for renewable diesel conversions is to help oil companies more cost effectively meet their obligations under the federal RFS and state fuel policies. The RFS requires companies selling gasoline and diesel to purchase biofuels to blend into the fuels they sell or else purchase credits from others who sell biofuels. The decision to convert an unneeded oil refinery to renewable diesel production facility reflects a decision that it is more cost effective to buy the feedstock and directly produce the fuel required for compliance compared to buying the fuel or associated credits from someone else. Selling renewable diesel in California also helps refiners satisfy the requirements of the California LCFS.

Finally, the conversion of a petroleum refinery to renewable diesel is attractive in part because it forestalls the need to begin a costly and complicated process of decommissioning an old refinery. UCS commissioned a recent report about lessons learned from the closure of a Philadelphia Oil refinery, which highlights how reluctant refiners are to close their refineries. A conversion to renewable diesel postpones the day of reckoning and gives the refinery owner more time to develop the most advantageous exit strategy.

The bottom line is that oil companies have a clear motivation to overstate the potential to convert oil refineries to biofuel production. The realistic potential for biofuel conversions is quite small because of the limited availability of suitable feedstocks. Exaggerated hype about potential for refinery conversions to biofuel production amounts to greenwashing that distracts from more scalable solutions.

Fuel markets are much bigger than feedstock markets

Securing adequate feedstock is a very different challenge than finding excess petroleum refining capacity. It is clearly not feasible for many states or the whole country match the rapid scaleup of bio-based diesel underway in California because the feedstocks are just not available. To produce 100 percent of 2022 US diesel fuel consumption in the transportation sector would require more than 160 million metric tons (MMT) of feedstock, which is 10 times US production of vegetable oils in 2022 or 80 percent of global vegetable oil production in 2022 (Source US Energy Information Administration, USDA Foreign Agricultural Service)[i]. To get a handle on the realistic potential for bio-based diesel, and the consequences of rapidly ramping up production, we need to explore the current and potential future supply of feedstock.

Where does the feedstock come from?

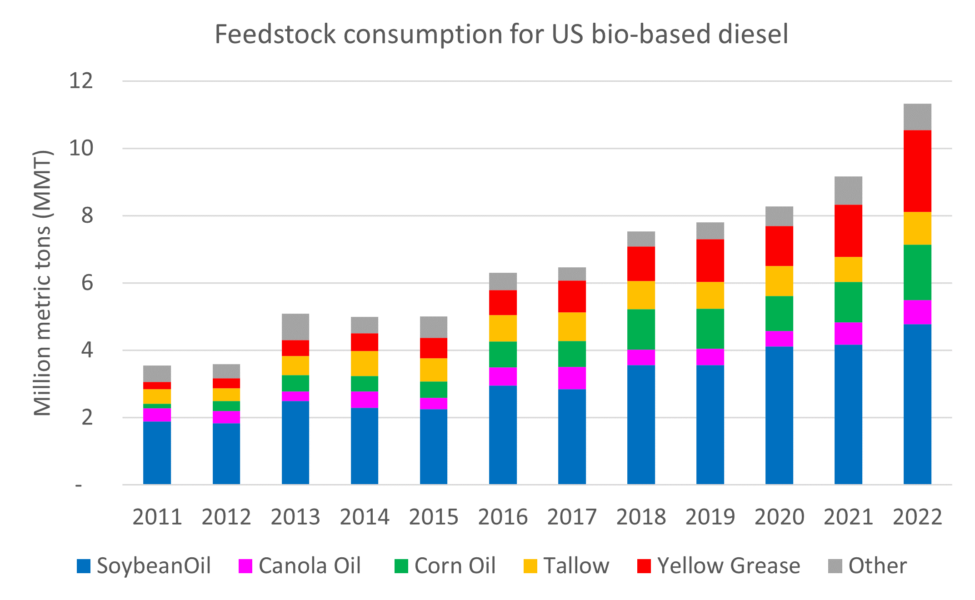

Figure 6, produced using data from farmdoc daily December 11, 2023, December 20, 2023, illustrates the feedstock used to produce the bio-based diesel fuels produced in the United States. Total feedstock consumption more than doubled in the last decade, exceeding 11 MMT in 2022. Imported bio-based diesel fuel consumed another 1.0 MMT of feedstock for fuel production abroad, so total US bio-based diesel consumption in 2022 required 12 MMT of feedstock, half of it to supply fuel to California.

Soybean oil is by far the most important source of bio-based diesel feedstock, accounting for almost half of the total. Combined with corn and canola oil, vegetable oils make up more than two thirds of feedstock. Yellow grease and tallow make up most of the remaining oil. Yellow grease includes used cooking oil and some other animal fats.

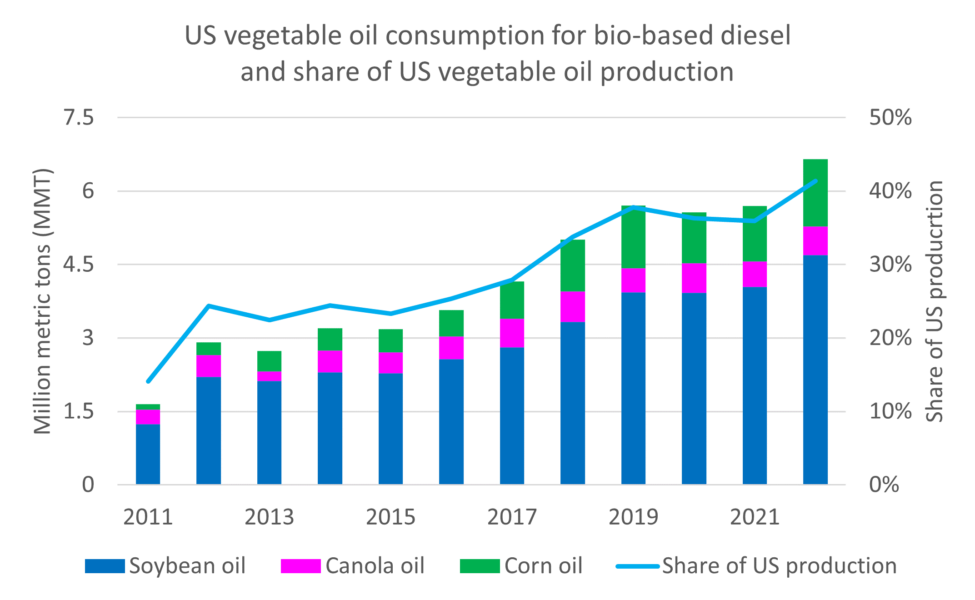

The US Department of Agriculture tracks the share of US vegetable oil production devoted to bio-based diesel, which has risen steadily and exceeded 40 percent in 2022.

Statistics for yellow grease, tallow and other feedstocks are less well documented, so it is hard to assign a precise share, but experts agree that a large share of the available resources are now being used to produce the bio-based diesel.

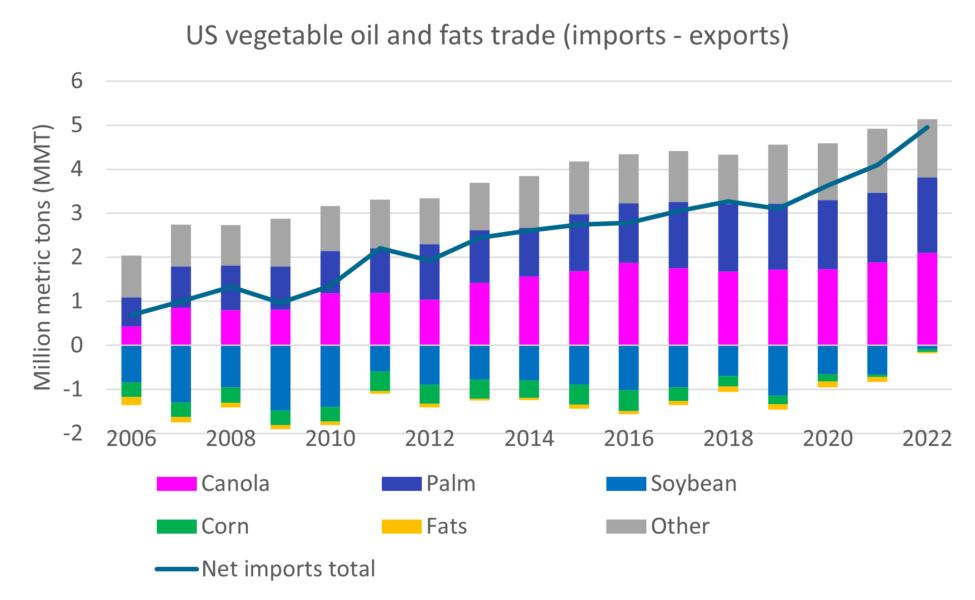

The growing share of US vegetable oil used for bio-based diesel production is reflected in the balance of US trade in vegetable oil. Net vegetable oil imports grew by about 4 MMT between 2006 and 2022, especially canola oil and palm oil, which have replaced soybean oil in food uses. This has been a gradual process that reflects both changing consumer preferences and diversion of soybean oil to fuel production. More recently the US has effectively exited the export market for vegetable oil entirely and is now the 4th largest importer of vegetable oil after India, China and the European Union (USDA Foreign Agricultural Service).

How much feedstock is needed for future bio-based diesel production?

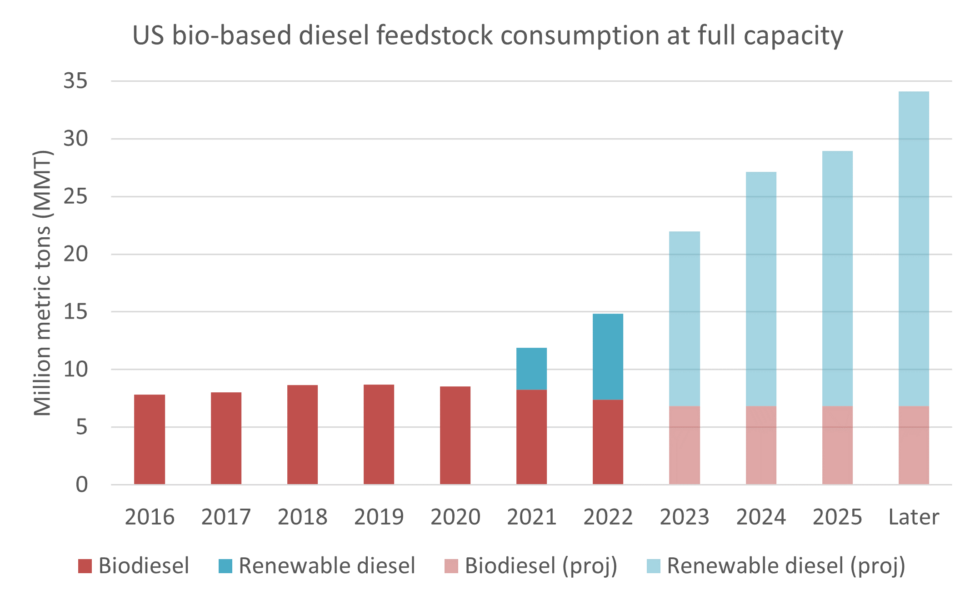

Scaling up bio-based diesel production requires more than production capacity; it also requires feedstock and demand. Figure 9 summarizes the quantity of feedstock that would be consumed if the planned renewable diesel facilities are built and operate at full capacity and the biodiesel industry continues to operate at its capacity as of the end of 2022. Capacity for feedstock consumption could rise by 10 to 20 MMT a year, or even more, a massive increase compared to the 11 MMT of actual US consumption in 2022. Declining production of biodiesel could potentially free up some feedstock for renewable diesel production, but since only 6 MMT of feedstock was used for biodiesel in 2022, even completely shutting down biodiesel production would free up just half of the feedstock required by renewable diesel capacity expansion announced for 2023 and 2024.

Where could an additional 10-20 MMT of feedstock come from?

The scale of demand for vegetable oil required to operate planned renewable diesel capacity is so large that meeting it would require dramatic changes to global markets for oils and fats with major implications for food consumers around the world and tropical deforestation. The bottom line is that palm oil is the only source of vegetable oil that could plausibly scale up to provide 10-20 MMT of additional vegetable oil in the next few years. Since palm oil is not an eligible feedstock for US biofuel production, other sources of oil, especially soybean oil, would most likely be diverted from food to fuel, while palm oil backfilled the soybean oil. It may seem absurd to even discuss increases this large, but analysis commissioned by a trade association for the renewable diesel industry argued recently that US feedstock for bio-based diesel could rise to 32 MMT in 2030, primarily from soybean oil.

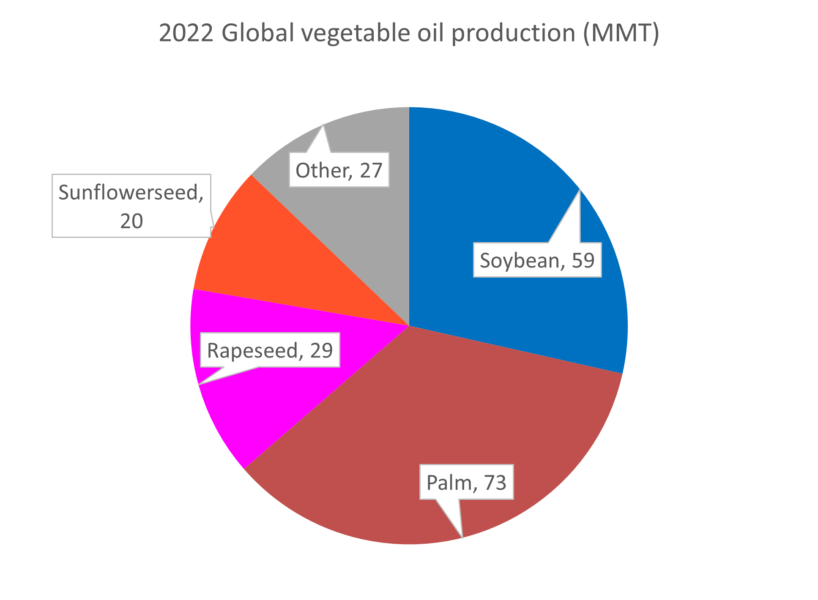

For a more detailed answer, please see this appendix. The main points are summarized below. Figure 10 shows global vegetable oil production in 2022.

Soybean oil accounts for three quarters of US vegetable oil production, and 29% of global production. and is the most plausible sources of supply for large increases in domestic production. To secure millions of metric tons of additional soybean oil, the US would need to reduce exports of whole soybeans and start importing soybean oil from Argentina and Brazil. If US oil companies are willing to outbid all other consumers, they could theoretically secure 10-20 MMT of additional RFS eligible feedstock. The bidding war would pit US oil companies against people’s food consumption. Over the longer term, oil crop cultivation would catch up with demand and stabilize prices. But because soybean oil is a joint product with soybean meal, it is not economic to expand soybean production faster than demand for soy meal as animal feed. Thus, the additional vegetable oil required to replace the soybean oil used for fuel will mostly come from palm oil, which together with soybean oil made up 64 percent of global vegetable oil production in 2022. Domestic production and imports of other oil crops like canola/rapeseed and increased imports of used cooking oil from around the globe can contribute a small amount. But at the scale of the biodiesel boom there is no plausible source of feedstock other than soybean oil backfilled in cost sensitive food markets by palm oil.

Advice to policymakers

The idea that oil refineries can keep humming along by replacing petroleum diesel with vegetable oil or used cooking oil is a dangerous illusion. Having US oil companies backed up by billions of dollars in direct and indirect subsidies compete on the global market for vegetable oil to make into fuel is an expensive dead-end that does not support investment in scalable low carbon technology but drives up food prices and ultimately serves mostly to expand the cultivation of palm oil to replace the soybean and other oils made into fuel.

When policymakers subsidize new technologies, the justification is often the potential that scaling up a new technology will lead to cost reductions over time. But producing soybean oil and refining it at existing oil refineries is not catalyzing any fundamentally novel technology, so there is no reason to expect breakthroughs in cost to result. Policymakers need to pay attention to where the vegetable oil and feedstocks for bio-based diesel fuels come from. And when policies are placing an unsustainable draw on scarce resources, they need to act decisively to limit feedstock utilization at a sustainable level.

Today the renewable diesel boom in California is at risk of becoming a crisis, and policymakers at the Air Resource Board must act now to stop the massive expansion of soybean oil-based renewable diesel. California officials should ensure that California does not use more than half the US supply of feedstocks for bio-based diesel and related fuels.

A comparison with electric vehicles in instructive. In 2016, California accounted for 50 percent of the registrations of passenger car EVs in the US. Since that time, EV registrations in California have grown 540 percent, but registrations in the rest of the US have grown even faster, so the share of EV registrations in California has fallen to 37 percent (Source: Alternative Fuels Data Center). Over the same timeframe, consumption of renewable diesel in California has grown almost as fast as EV registrations, up 440 percent between 2016 and 2022. But where early action by California policymakers led to reduced cost and increased availability of EVs elsewhere, California’s appetite for bio-based diesel feedstocks led to a decline of bio-based diesel consumption in the rest of the United States, with US consumption of bio-based diesel outside of California falling 19 percent between 2016 and 2022. The biodiesel boom is increasing costs and decreasing availability of renewable diesel and biodiesel in the rest of the United States and if the boom in California is not contained, it will lead to disruptions of global vegetable oil markets and accelerate tropical deforestation. More details on UCS’s proposals to reform the Low Carbon Fuel Standard can be found here.

Ultimately, excessive utilization of any source of biofuel can become a problem if exploited at an unsustainable level. Biofuels can play a productive role if the crops used to produce them are grown without displacing food production or expanding the footprint of agriculture onto sensitive ecosystems. Policymakers need to be realistic about where biofuels come from, and limit feedstocks to a sustainable scale to avoid sending our fuel policies down a damaging dead-end road.

[i] In the discussion of feedstock requirements I make a few simplifying assumptions about conversion rates and report everything in millions of metric tons (MMT). My estimates are based fuel consumption data from EIA reported in gallons and assuming 7.55 pounds of feedstock per gallon for biodiesel and 8.125 pounds per gallon for renewable diesel, consistent with farmdoc daily, May 1, 2023. Actual values will vary by feedstock, conversion process and facility, but this should be a reasonable and consistent approximation.